Blog

To Infinity and Beyond: A Guide to Taxation of Cross-Border Services in the Philippines

Benjamin Franklin’s famous quote, “in this world, nothing is certain except death and tax,” takes on a whole new spin as the Supreme Court recently tackled the taxation of literally out of this world activities in the 2022 case of ACES Philippines vs. Commissioner of Internal Revenue (ACES Philippines ruling).1

The ACES Philippines ruling, to continue the pun, is now causing cosmic ripples to the income tax treatment of the services rendered by foreign international service providers (ISPs) in the Philippines, especially considering the recent issuances of Bureau of Internal Revenue (BIR) Revenue Memorandum Circular (RMC) Nos. 05-20242 and 38-2024.3

One legislator even raised the concern that RMC No. 05-2024’s imposition of 25% final withholding tax and 12% value-added tax to cross-border services, if not properly delineated, can erode the Philippines’ competitiveness in attracting foreign investors.4

To extract lightsaber-sharp cutting guidelines, a telescopic view of the ACES Philippine’ ruling and BIR RMC Nos. 05-2024 and 38-2024 is called for.

The Rule Established in ACES Philippines Ruling

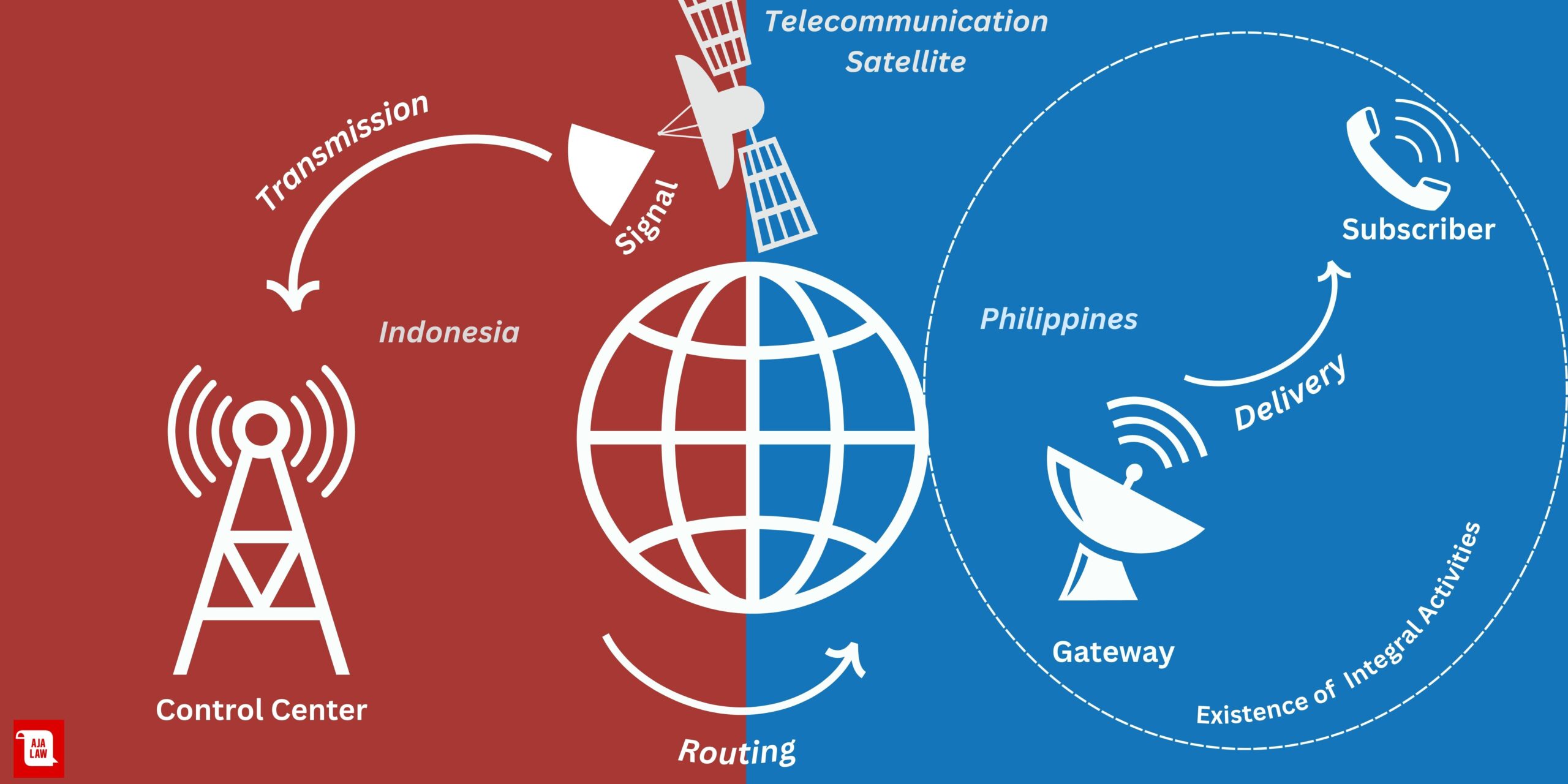

As mentioned, ACES Philippines involves in and out of this world activities divided into three different stages, as illustrated in the itemized stages and diagram below:

- A Non-Resident Foreign Corporation (NRFC), ACES Bermuda owns a telecommunications satellite in outer space with a network control center located in Indonesia.

- This satellite transmits radio signals from and to its earth stations or “gateways.”

- Upon transmittal to a Philippine gateway, ACES Philippines then processes and routes the signals to its end-users or subscribers.

Pursuant to their Gateway and Airtime Purchase Agreements, ACES Bermuda thus charged ACES Philippines for the use of its satellite transmissions and airtime but insisted that its airtime services were all rendered outside the Philippines. However, the Supreme Court classified ACES Philippines’ payment as ACES Bermuda’s income sourced within the Philippines based on two distinguishing features of these transactions: (1) the Philippine gateways’ receipt of the routed signals, and (2) the delivery of the routed signals as airtime calls for utilization by Philippine subscribers.

Notably, ACES Bermuda charged airtime fees only upon utilization by Philippine subscribers; unanswered calls were excluded from these agreements.

The decisive point in determining the taxability, therefore, is the place of the revenue-generating activity or, in the words of the Supreme Court, the place where the inflow of wealth and/or economic benefits proceeded from which, in this case, was the utilization of airtime calls. This is also called the “benefits-received theory” of income taxation which was later adopted in the RMCs discussed here.

Coverage and Test under RMC No. 05-2024

Following the ACES Philippines’ ruling, BIR issued RMC No. 05-2024 to provide a laundry list of similar cross-border services, namely: consulting, IT outsourcing, financial, telecommunications, engineering and construction, education and training, tourism services. And as a catch-all definition, BIR defined other similar cross-border services as services: (1) being provided, processed, or performed overseas, and (2) then utilized, applied, executed, or consumed within the Philippines.

To ascertain income as a Philippine-sourced income for purposes of ISPs, BIR adopted the essentiality or integrality test, which requires an examination whether activities or stages taking place within the Philippine territory are so essential or integral, that the income-generating activity will not be realized without it. If found essential or integral, then the income for the said activity shall be considered sourced from the Philippines. This ensures that different jurisdictions maintain their tax base, impose the appropriate taxes, and prevent tax avoidance.

Factors for Applicability and Other Considerations in RMC No. 38-2024

Considering the comprehensive list of cross-border services mentioned in RMC No. 5-2024, BIR issued RMC No. 38-2024 to clarify that the entirety of the cross-border services must be examined to determine the source of income.

And once established that the source of income is within the Philippines, a NRFC, within a foreign territory with a Philippine tax treaty, may still invoke for tax exemption or preferential, especially in the absence of a permanent establishment in the Philippines, as defined in the tax treaty of their respective state.

Finally, income derived from services provided by foreign companies, which are deemed sourced within the Philippines, is subject to not only final withholding taxes but also value-added tax; as the term “sale or exchange of services” within the contemplation of Section 108(A) in relation to Section 114 of the Tax Code encompasses various activities, including any service rendered within the service fees paid to foreign entities or individuals.

Course of Action for Cross-Border Service Providers

Considering the ACES Philippines’ ruling and RMC Nos. 5-2024 and 38-2024, we highly encourage foreign investors and their local partners to conduct a meticulous review of their current and future cross-border service agreements to ensure taxes, when and where due, are timely paid and tax treaty exemptions are duly raised.

If you require legal guidance on your matter or situation

Work WITH OUR TEAM

Prepared by Thea Ruth L. Magallanes and Reinalyn L. Domasig.

FOOTNOTES

- G.R. No. 226680, August 30, 2022.

- Revenue Memorandum Circular No. 05-2024, Further Clarifying the Proper Tax Treatment of Cross-Border Services in light of the Supreme Court En Banc Decision in Aces Philippines Cellular Satellite Corp. v. Commissioner of Internal Revenue, G.R. No. 226680, dated August 30, 2022.

- Revenue Memorandum Circular No. 38-2024, Clarifying the Issues Raised on Revenue Memorandum Circular No. 5-2024.

- Paunan, Jerome Carlo, Gatchalian seeks Gatchalian seeks inquiry on BIR imposition of 25% withholding tax, 12% VAT on cross-border services (published April 01, 2024), available at https://pia.gov.ph/news/2024/04/01/gatchalian-seeks-inquiry-on-bir-imposition-of-25-withholding-tax-12-vat-on-cross-border-services (last accessed April 05, 2024).